Day 27: Enhancement

On Day 26, we extended the comparative error analysis to the original, 12-by-12 strategy and showed how results were similar to the unadjusted strategy relative to the adjusted one. The main observation that emerged was that the adjusted strategy performed better than the others due to identifying most of the big moves when it was correct and not missing the big moves when it was not. This was borne out by statistical tests that showed the mean difference between returns for the true positives and false negatives for the adjusted strategy were indeed significant relative to the others. We also noted, rather coyly, that we had one more enhancement to the strategy. Let’s discuss that now.

Recall, the adjustment we use adds the derivative of the loss function with respect to the prediction on a single out-of-sample test to next available prediction. We hypothesized that it tended to succeed because it likely prevented the directional prediction from the successive walk-forward models from reverting too quickly in the near term. The directional prediction of the models will tend to be in the (modestly) opposite direction adjusted for the intercept (which is roughly speaking the mean of the actual).1 However, only when the lookback returns are sufficiently large to offset the intercept will the directional prediction actually change from the average of the prior lookback returns. When we add the error correction term it only changes the sign if it is sufficiently larger in absolute terms than the prediction and of the opposite sign. But we don’t know if it is sufficiently large without iterating a range of values.

What if we multiplied the error term by the prediction instead? In this case, the directional predictions would skew toward the positive and only on those occasions where the prior prediction was less than the actual would the sign flip.2 Doing that produces the following cumulative return chart.

In this case, the new adjusted strategy performs significantly better! It outperforms buy-and-hold and the original strategy by 36% and 26% points, respectively. It enjoys almost twice the cumulative return as the unadjusted strategy. Critically, the new adjusted strategy’s Sharpe ratio is almost double that of buy-and-hold at 0.6 and 0.08 points better than the original. If we had implemented short-selling, the strategy would have performed even better.

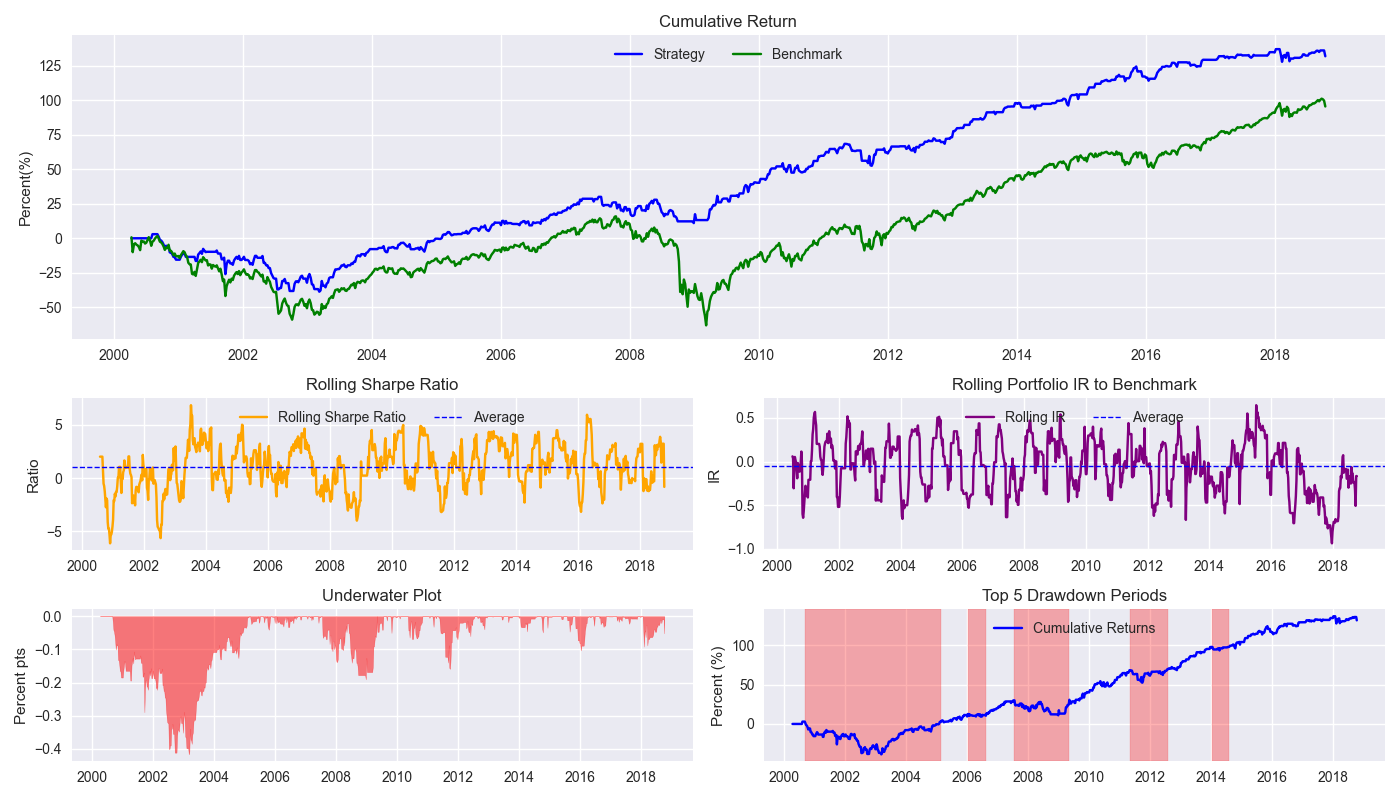

When we plot the various metrics in our handy tearsheet (below) against buy-and-hold, we note that new adjusted strategy suffers similar drawdown periods as the original strategy, but the main advantage appears to be avoiding the really large down moves. Indeed, the new adjusted strategy is out of the market almost 5% more than the original strategy. We’ll present the remaining metrics we’ve used and run the circular block sampling in our next post. After that we come to the pièce de résistance – testing the finished model on out-of-sample data. Stay tuned!

Code below.

# Built using Python 3.10.19 and a virtual environment

# Load packages

import pandas as pd

import numpy as np

from datetime import datetime, timedelta

import statsmodels.api as sm

import matplotlib.pyplot as plt

from matplotlib.ticker import FuncFormatter

import yfinance as yf

import seaborn as sns

from scipy.stats import ttest_ind

plt.style.use('seaborn-v0_8')

plt.rcParams['figure.figsize'] = (14,8)

def get_spy_weekly_data() -> pd.DataFrame:

df = yf.download('SPY', start='2000-01-01', end='2024-10-01')

df.columns = ['open', 'high', 'low', 'close', 'adj close', 'volume']

df.index.name = 'date'

# Create training set and downsample to weekly ending Friday

df_train = df.loc[:'2019-01-01', 'adj close'].copy()

df_w = pd.DataFrame(df_train.resample('W-FRI').last())

df_w.columns = ['price']

return df_w

df_w = get_spy_weekly_data()

# Create momentum dictionary

periods = [3, 6, 9, 12]

momo_dict = {}

for back in periods:

for forward in periods:

df_out = df_w.copy()

df_out['ret_back'] = np.log(df_out['price']/df_out['price'].shift(back))

df_out['ret_for'] = np.log(df_out['price'].shift(-forward)/df_out['price'])

df_out = df_out.dropna()

mod = sm.OLS(df_out['ret_for'], sm.add_constant(df_out['ret_back'])).fit()

momo_dict[f"{back} - {forward}"] = {'data': df_out,

'params': mod.params,

'pvalues': mod.pvalues}

# Trade with error handling

df_trade_1 = momo_dict['12 - 12']['data'].copy()

mod_look_forward = 12

train_pd = 5

test_pd = 1

tot_pd = train_pd + test_pd

lr = 2

trade_pred = []

trade_pred_un = []

trade_pred_old = []

for i in range(tot_pd, len(df_trade_1)-mod_look_forward+1, test_pd):

train_df = df_trade_1.iloc[i-tot_pd:i-test_pd, 1:]

valid_df = df_trade_1.iloc[i-test_pd:i, 1:]

uncorr_df = df_trade_1.iloc[i-test_pd+mod_look_forward-1:i-test_pd+mod_look_forward, 1:]

test_df = df_trade_1.iloc[i-test_pd+mod_look_forward:i-test_pd+mod_look_forward+1, 1:]

# Ensure 'ret_back' is 2D by selecting it as a DataFrame, not a Series

X_train = sm.add_constant(train_df[['ret_back']])

if valid_df.shape[0] > 1:

X_valid = sm.add_constant(valid_df[['ret_back']])

else:

X_valid = sm.add_constant(valid_df[['ret_back']], has_constant='add')

if uncorr_df.shape[0] > 1:

X_uncorr = sm.add_constant(uncorr_df[['ret_back']])

else:

X_uncorr = sm.add_constant(uncorr_df[['ret_back']], has_constant='add')

if test_df.shape[0] > 1:

X_test = sm.add_constant(test_df[['ret_back']])

else:

X_test = sm.add_constant(test_df[['ret_back']], has_constant='add')

# Fit the model

mod = sm.OLS(train_df['ret_for'], X_train).fit()

# Predict using the test data

pred = mod.predict(X_valid).values

actual = valid_df['ret_for'].values

gamma = -(actual - pred)*lr

pred_old = mod.predict(X_uncorr)

trade_pred_old.extend(pred_old)

mod_pred = mod.predict(X_test).values

trade_pred_un.extend(mod_pred)

trade_pred.extend(mod_pred * gamma)

assert len(trade_pred) + mod_look_forward + train_pd == len(df_trade_1)

assert len(trade_pred_un) + mod_look_forward + train_pd == len(df_trade_1)

df_trade_1['pred'] = np.concatenate((np.zeros(mod_look_forward + train_pd), np.array(trade_pred)))

df_trade_1['pred_un'] = np.concatenate((np.zeros(mod_look_forward + train_pd), np.array(trade_pred_un)))

df_trade_1['pred_old'] = np.concatenate((np.zeros(mod_look_forward + train_pd - 1), np.array(trade_pred_old), np.zeros(1)))

df_trade_1['ret'] = np.log(df_trade_1['price']/df_trade_1['price'].shift(1))

df_trade_1['signal'] = np.where(df_trade_1['pred'] > 0, 1, 0)

df_trade_1['signal_un'] = np.where(df_trade_1['pred_un'] > 0, 1, 0)

df_trade_1['signal_old'] = np.where(df_trade_1['pred_old'] > 0, 1, 0)

df_trade_1['signal_sh'] = np.where(df_trade_1['pred'] >= 0, 1, -1)

df_trade_1['strat_ret'] = df_trade_1['signal'].shift(1) * df_trade_1['ret']

df_trade_1['strat_ret_un'] = df_trade_1['signal_un'].shift(1) * df_trade_1['ret']

df_trade_1['strat_ret_old'] = df_trade_1['signal_old'].shift(1) * df_trade_1['ret']

df_trade_1['strat_ret_sh'] = df_trade_1['signal_sh'].shift(1) * df_trade_1['ret']

# Plot returns

(df_trade_1[['strat_ret', 'strat_ret_old', 'ret']].cumsum()*100).plot()

plt.ylabel("Return (%)")

plt.xlabel("")

plt.legend(['Corrected', 'Original', 'Buy-and-Hold'])

plt.title('Cumulative returns: 12-by-12 Strategy (with and without error correction) vs. Buy-and-Hold')

plt.show()

# Tearsheet

# For plot_tearsheet function

# See https://www.optionstocksmachines.com/post/2024-11-08-day-16-comps/

plot_tearsheet(df_trade_1['strat_ret'], df_trade_1['ret'], window=13, period=52, save_figure=False, title=None)Since the OLS regression equation is given by: \(\hat{y} = \beta_{0} +\beta_{1}x_{1}\)

Taking the mean of both sides yields \(\bar{\hat{y}} = \beta_{0} +\beta_{1}\bar{x_{1}}\)

Note: the mean of the prediction will tend to equal the mean of the actual. Hence: \(\bar{\hat{y}} = \bar{y}\)

Also the mean of \(\beta_{0}\), is just that, since the data is a vector of ones.

Thus the intercept is basically the mean of the actual less the mean of the independent variable times its coefficient.

\(\beta_{0} = \bar{y} - \beta_{1}\bar{x_{1}}\)

Since \(\beta_{1}\bar{x_{1}}\) is likely to be relatively small (a fraction times a fraction), the mean of the actuals roughly approximates the intercept.↩︎

Whenever the actual is greater than the predicted value the error correction will have a negative sign. When less than, a positive one.↩︎